Holiday money is one of the fundamental things you’ll need when travelling. This post covers the different options to choose from to ensure you’re prepared for your trip.

These are my personal opinions – I do not receive any commission or gains from recommending the companies or products in this article.

Page contents

Credit Cards

One of the easiest ways to spend your holiday money, is using a 0% foreign transaction credit card. When you don’t have to pay additional fees to spend your money in a different currency, you’ll get the best rates. Credit cards also come with a range of protection options. They are my default method for spending abroad.

While I collect points, sadly most points earning credit cards add a charge of up to 3% for any foreign transactions. Sometimes I still use them because the points received outweigh the charge, but I also have two 0% credit cards. The two cards I use; Nationwide Select Credit Card and JAJA Credit Card; are not currently accepting new applications, however there are several other credit cards available with 0% overseas fees.

Money Saving Expert (MSE) is a UK site which helps you save money on so many things, including travel. I’ve often used it to check for the current best market options for different cards. MSE constantly updates information, so you’ll get the best 0% credit card recommendations at the time. Just check that the card recommended fits with your personal circumstances.

AWTT Tip – You shouldn’t use Credit cards to make cash withdrawals abroad. You’ll be charged a transaction fee as well as interest at the cash rate. Furthermore, it could hurt your credit score. It’s better to take out cash from a debit card with no charges.

If you can, do a bit of research into your chosen destination to see how widely credit cards are accepted. If you’re in the UK, check out the Foreign, Commonwealth & Development Office (FCDO) travel information. This site covers basic details regarding access to money for most countries. For example, the advice for Mauritius is that ATMs are in most towns and shopping centres, with credit/debit cards widely accepted in hotels, restaurants and retailers. However, for Vietnam the advice is that credit cards are widely accepted but to carry cash in rural areas, and ATMs are available in major cities/tourist spots.

Looking up this sort of information in advance will help you plan the best options for your holiday money.

- Related AWTT Content:5 things you’ll need for every trip

Debit Cards

Another good option for your holiday money is to bring at least one debit card with you on your travels. If you have a debit card offering 0% on both foreign transactions and withdrawals this is a solid choice. It will enable you to pay for purchases on the card, but also give you the flexibility to withdraw cash should you need some. Below are some good options that I personally use.

Starling Bank

Starling Bank is an online only bank for individual or joint accounts, with a great travel package. It’s really easy and quick to set-up and has great in-app features, like being able to freeze your card instantly if its lost or stolen. Starling Bank is has £85,000 cover with the Financial Services Compensation Scheme (FSCS) like most traditional banks.

I personally use this account and love the flexibility it offers. Using a phone banking app means I have access to my money wherever I have Wi-Fi (using a VPN of course). You can use your Starling card to make free cash withdrawals in overseas ATMs, as well as debit card transactions.

A feature I really like in Starling’s app is the ability to have “spaces”. These are separate ‘saving pots’ where you can put money aside for any purpose (mine are all holiday pots) and it keeps it separate from your main account balance. This is useful in case your card is stolen as they can only access your main balance, not your savings. You can transfer money manually to your “spaces” as well as rounding up your normal spending to save faster. It won’t cost anything to move money between your “spaces” and your main account. You can also set targets and add pictures so you can see what you’re saving for and your progress towards your goal.

Starling Bank have great customer service and I find everything very easy to use. I’d thoroughly recommend signing up for an account, even if you only use it for travel.

Monese

Another online banking provider which offers decent travel perks is Monese. A digital only banking service, it’s simple and straightforward to apply through their app. You can use your Monese card internationally, and depending on the card you have, you’ll get different allowances for spending or withdrawing cash.

At present (April 2021) you’ll be able to choose from three different card options:

- Simple (free card) – allows £200 cash withdrawal per month (2% fee afterwards) and £2000 foreign currency spending.

- Classic (£5.95 per month) – allows £900 cash withdrawal per month (2% fee afterwards) and £9000 foreign currency spending.

- Premium (£14.95 per month) – allows unlimited free cash withdrawal and foreign currency spending.

Your able to upgrade or downgrade your card, so you won’t be tied into a plan if it becomes unsuitable. The features available allow you to see a spending overview as well as transaction details, and with everything being in the app you have complete control at your fingertips.

The simple free card is sufficient for my needs, as I use my Starling card in the first instance and have my Monese card as my backup if I have any issues.

![]()

Curve

The Curve card is a new discovery for me, but it’s not a bank! You connect your existing credit and debit cards, and then only need to carry the Curve debit card with you to use for any transactions. There’s also the option to upload your Curve card to Apple, Google or Samsung Pay and avoid the need to carry any cards with you.

Curve offers three different cards and they have other perks in addition to the travel benefits, including cashback offers and money for referring friends to Curve. The card I have is Curve Blue, ‘the classic’ or free card. Curve Black is ‘the premium’ card which costs £9.99 per month. They also have ‘the ultimate’ Curve Metal card which has the most features for £14.99 per month.

Key travel benefits for the free Curve card include:

- Free cash withdrawals up to £200 per month, with a 2% or £2 charge (whichever is higher) if you go above that amount.

- £500 per month 0% fee on spending, with a 2% charge for any additional spending.

Important details

You can only connect Visa and Mastercard credit and debit cards to your Curve account but can use them for card transactions or cash withdrawals. Just be sure to check your credit card T&Cs as some cash withdrawals using Curve will be charged interest.

Your Curve card will also have a maximum daily spent cap which will be detailed in the app. This might be more or less than the underlying linked card limit.

The Curve app is where you choose which of your linked cards will be charged, and this can be done ahead of any transactions. Alternatively, Curve has a unique feature called Go Back in Time. It enables you to switch the payment card used for the transaction up to 90 days after the payment has been made!

This is a very way of banking and I’m loving it! Especially the Go Back in Time feature, which I’ve used to move transactions made using a non-points credit card, over to my Virgin Atlantic Reward+ Credit Card to maximise my points collection!

![]()

Other Debit Cards

There are lots of other good travel debit card options, such as Virgin Money, Currensea, Monzo and Nationwide FlexPlus to name a few. Check them all out and find one that suits you. Just be mindful that not all debit cards are equal, and some will sting you for cash withdrawals and overseas transactions.

- Related AWTT Content: The Power of 3: How to pack light for every trip

Prepaid Cards

Prepaid cards are a good idea if you want or need to stick to a budget. You load a chosen amount of money onto the card before you travel, and then use the card either for payments or to withdraw cash. You’ll have the option to top-up the card at any point if you do need more holiday money.

At the time of loading your money you can lock in the exchange rate. Otherwise, you can choose to pay in pounds, and you’ll get whatever the exchange rate is on that day. The Fair FX card is one of the leading prepaid card options, but this site gives a helpful comparison of several prepaid cards.

![]()

There are some downsides to prepaid cards to be aware of. Firstly, they often have some fees, whether that is for using the card (fee transactions), application or postage charges for the card, or to keep the card active. Secondly, prepaid cards are not usually as widely accepted as credit or debit cards, for example you can’t use them as a payment method to hire a car.

I’ve used a prepaid card for some of my past trips (which is no longer available) as it was easy to reload whilst travelling and meant all my money wasn’t in one location. However, I’ve switched to using credit and debit cards as they have better rates and benefits overall.

Foreign Cash

Cash is probably the most widely accepted form of holiday money. It’s not always the most secure, but it’s usually useful to have some (either notes or coins), particularly if you’re visiting somewhere off the beaten track. There are several ways to get foreign currency.

Prior to departure

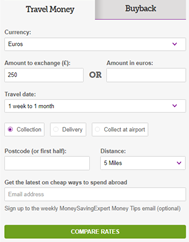

Getting foreign currency ahead of your trip can be one of the easiest ways, as you’ll have it ready as soon as you need it. Rates across the UK can vary but I’ve used Travel Money Max from Money Saving Expert (MSE) whenever I’ve wanted to get foreign cash in advance.

Just enter the currency you want, and then select either the amount you want to exchange in pounds or the amount of foreign money you want. Then choose if you want the currency delivered to you, or if you prefer to collect from a location, including at an airport. Also select when you’ll be travelling – sometimes the rate will be better if the currency isn’t needed urgently. Travel Money Max will then show you a comparison of different rates from a range of providers.

The site also offers comparisons for firms that will buy back currency if you have any left over after your trip.

AWTT Tip: You’ll usually find airport exchange rates are lower – you’re better off getting your cash before going to the airport or waiting until you arrive at your destination.

At your destination

My preferred method to obtain holiday money is to make an ATM withdrawal on arrival in the airport. This way I avoid carrying additional cash with me from home to the departure airport, and whilst on the plane.

Using one of the debit cards above, avoids direct banking charges to take out cash, but be careful as some ATMs will still have their own usage fee. If one ATM has a fee, I’ll usually try another first. Just be mindful that any fees might not be specified until the end, after the withdrawal amount has been selected. If there is a fee, I take out a larger amount of cash to avoid too many transaction fees.

One downside to waiting until you arrive, is that it can be difficult to know what the exchange rate will be. This means there is a chance you will get a less competitive rate than getting cash in advance, but in my experience it’s not a huge difference.

Another way to get cash besides ATMs is through a Travel Bureau. However, there are so many stories where people have been ripped off by the exchange rates. Or they are caught out by scams which focus on confusing or distracting travellers. I therefore tend to avoid getting cash out via this method.

I always spend time during my trip planning to investigate money preferences. It helps knowing if cash will be needed or whether card payments are accepted everywhere. Doing so means I only take out a small amount of cash, particularly if the exchange amount means a lot of bank notes. For example, when I visited Bali in 2019, I withdrew £100 cash on arrival and became a millionaire!

With free withdrawals through my Starling card, I’m able to make further withdrawals as and when needed. This way I’m not carrying massive amounts of cash on me, which could be risky.

- Related AWTT Content: 10 useful tips for your first visit to Bali

Travellers Cheques

Travellers cheques are a secure alternative to carrying cash. You get pre-printed cheques with a designated amount that you then use to pay a retailer. If the cheque balance is higher, you’ll get your change in the local currency.

As well as being more secure than cash, each one has a unique reference number. Therefore, you can cancel the cheque if it’s lost and get your money back. Also, there’s no expiration on undated cheques, but once you add the date, they need to be used within six months.

However, this method of holiday money is gradually becoming a thing of the past, with the rise of easier to use credit and debit cards. You can still get travellers cheques in some places such as banks and post offices.

There are a couple of things to be mindful of when it comes to travellers cheques. The first is that there is usually a transaction fee required to exchange them. The second is that they may not be widely accepted in your holiday destination. If you want to use them as a payment method, it would be worth checking in advance.

Conclusion

Ultimately, I find the best option for holiday money is a combination of credit cards, debit cards and foreign cash. Choosing a combination of cards and cash gives you flexibility when travelling. Plus, you’ll have a better level of security in case something unfortunate happens.

Travel planning can also help you decide the best way to obtain your holiday money. Some places you may only need to pay by card, but in other countries cash might be preferred.

For me personally, I usually have two or three credit cards, two debit cards and sometimes some cash as well.

Things To Remember

- Ensure you keep your different cards/cash in a couple of different locations. It’s good practice in case something happens and means you won’t be without access to funds.

- Choose to pay in the local currency when using your credit or debit card. Doing so means your card company makes the conversion, which will usually be a far better rate than the retailer.

- Use an RFID (radio frequency identification) sleeve or wallet/purse. These protect your cards from being cloned whilst in your bag, plus you can get larger ones for your passport. You can get them for a reasonable price on Amazon.

- Research your chosen destination to check whether there is a preference for cards or cash. For my Iceland trip I read they hope to become a cashless society, so I used my credit card everywhere!

- Have more than one option! I cannot stress this enough – please don’t rely on just one holiday money option. I recommend taking at least two cards if possible. You never know if an ATM might reject one of your debit cards, or it could be lost or stolen.

- Related AWTT Content: 13 spectacular waterfalls in Iceland that will amaze you